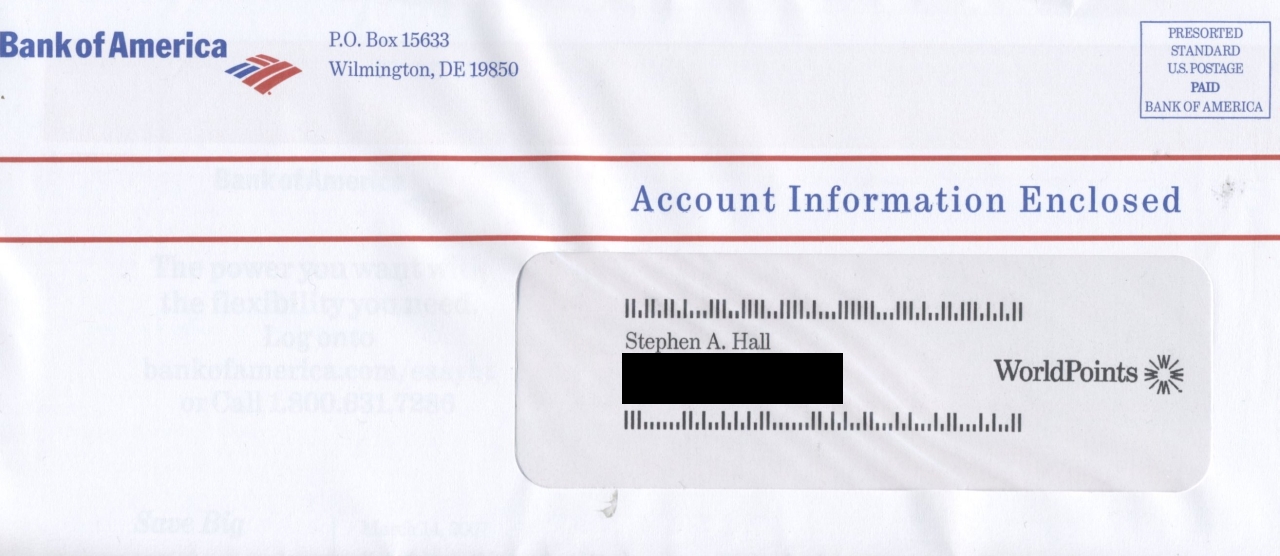

Bank of America Direct Mail Misleads

No, Bank of America (and all other financial institutions for that matter), my account information is not enclosed in this letter. In case you hadn't read your own mail before sending, what's contained inside this letter is not my bank statement but rather yet another offer for me to consolidate debt, spend more money on a vacation and create even more debt by writing a check against my credit card account to spend frivolously on things I don't want or need.

Perhaps direct mail guru Bob Bly can put my mind to rest. Has it become permissible for the practice to mislead, lie and misinform as standard practice? I never created email that lied and for years I've ignored this idiocy. I can't any longer. It's bad enough Bank of America requires you to have a degree in accounting to figure out how much you actually owe on your overdraft account. Now they want you to go deeper into debt with these idiotic monthly offers. Yes, of course, I ignore all of them but after 24 months of me not responding, you think they'd want to save a stamp or two. Oh wait, direct mailers don't care about the wasted 98 percent of people who ignore their offers.They only care about the two percent that respond. Silly me.

Comments

Is this true about the 2% response to direct mail? I knew it was low but not that low. Why would an advertiser participate in something that was so ineffective?

Ineffective? Based on what criteria? If the profit an advertiser makes on that 2% more than makes up for the cost of the whole mailing, then it makes that mailing very effective.

Scott Payne, you are an idiot.

I'd like to think that I don't send junk mail, but that's why I will never take a job in financial services, insurance, etc (I work in hospitality and want to keep it that way). Regardless, 3% is considered good, 1-2% considered standard (and will likely make up the cost of the mailing), so yes, we'll keep sending mail because some people do respond.

I may have mentioned this before, but the real key to getting past all the "misleading" crap on the front is to look at the postal indicia. See how it says "Standard Mail?" Any correspondence that contains actual identifying information other than a name and address (a customer ID, SSN, etc) must be sent via first class. So one quick look at the indicia and you'll know if it should go right past the shredder and directly into the recycle bin.

To my direct mail bretheren: sorry to have busted you, but maybe you should get more creative to get people to open then envelope anyway. Or send first class, you cheap bastards.

Mmmmm..."indicia." Now that's word I haven't heard in a long.

Sigh. The flood of memories...

To Lesley's point -- that's why some of them tip those faux plastic credit cards on the letter. But I agree that's still more sneaky BS that most of the time the client insists on having. As someone who writes tons of credit card DM shit for a nameless mega-bank, I find that the only creative way to get someone to open the envelope is to make the offer as compelling as possible. If that means screaming 0% APR and all that, so be it.

I believe that consumers are beginning to feel what I call "credit fatigue." The market is over-saturated as banks keep rolling out card after card every year. We're sick to death of it clogging our mailboxes, and are becoming much more wary about taking on additional financial obligations. For the better, too. That credit card offer now has to compete not only with the rash of other card offers and other junk mail detritus, but also against our growing antipathy for acquiring more debt. Or at least against other more positive forms of debt, like mortgages and college loans.

But Steve, in your case, where you already have an existing relationship with BoA, it has to be somewhat vague by law. The bank can't communicate on the envelope the fact that you have an account with them because of privacy issues. Notice that they never say "Your account information enclosed" or "Your statement enclosed". And saying "Checks to write against your credit card account enclosed " is, natch, verboten.

The reason why Bank of America sent you a letter to CONSOLIDATE DEBT and entice to into EVEN MORE DEBT is b/c they are damn (yet unethical) smart marketers. You ended up on a list that showed you had bad credit and they had an opportunity to put you even further into debt. They know how to market their database. They know more about your spending behavior with an Experian pull and modeling than you even know about yourself.

And they are enticing you with the "stuff you don't want or need" (and @ idiotic monthly offers that they assume you will eventually default on) b/c that is the very stuff that has put you in the position to be receiving these offers. When you start start receiving this shit (especially via Standard A - which means "we don't give a poop about you") - call a credit counselor.

Sorry to post this - but this is DATABASE Marketing 101 - delivered via direct mail. This has nothing to do with the stupidity of direct marketing. Done right (with proper database modeling) it can be genius).

The trouble with that line of thinking, psugirl, is that I don't have much debt. Aside from a mortgage which I pay on time along with all my other monthly bills, I'm far from the picture of financial idiot.

Then this mailing makes even more sense. Steve, you probably have a high credit score, which means that the risk of you defaulting on additional credit is low, so Bank of America will want you take on additional debt (and with them, so they can make fees on it). Makes perfect sense.

I agree that the BS sleazy marketers put on the outer envelope to get you to open it is annoying (recall the "YOU HAVE JUST WON ONE TRILLION DOLLARS...maybe"). But not all marketers are like that. Actually, I think Bank of America is really the worse (when I got a mortgage with them, I kept receiving junk mail with "Important Mortgage Information Update Enclosed" but they were just Bank of America credit card offers or some shit like that).

But what drives me even more crazy is when people bitch and complain about all the junk mail they receive. If you don't like it, then sign up with the DMA's do-not-mail list. That will save the companies money in that they won't waste resources mailing to someone like you who will never respond anyways.

I'm a current Bank of America customer, and it's worth noting that on literally every bit of junk mail I get from them (and they DO send a lot), there is a notice to opt-out of pre-screened mailings.

I didn't recieve the one Steve Hall did, but I bet that language is in there. I find the mail annoying, too, not annoying enough, apparently, to go out of my way to opt out of it.

Another thing to take away from all this is that despite the junk mail, I still think BoA is probably the best large bank in the country as far as fees, account features, and perks. They outright gave me $30 free last year as a side effect of using the "Keep the Change" feature. Show me another bank that gives me money for making it easier for me to save. (And no, I don't work for or with BoA.) They can send me all the junk mail they want if they keep giving me $30 a year.

Deja vu all over again. BofA keeps mailing this piece because it works, plain and simple. (And BTW, someone is guessing at that 2% rate, because I don't think BofA is announcing their response rates in the NY Times...)

As for getting incensed about it, this reminds me of the mailings we used to send for magazine subscriptions that went out in a plain tan Kraft paper envelope with no teaser copy, just a very official-looking bold type notice that said: ATTENTION, POSTMASTER! IF UNDELIVERABLE, PLEASE HANDLE ACCORDING TO U.S. POSTAL REGULATION NO. (or whatever). Of course, "Postal Regulation" was real, but was only the direction to throw away undeliverable third class (bulk rate) mail. And speaking of bulk rate mail, a printed postal indicia is not a dead giveaway, as someone said above: some mailers use first class stamps, some use bulk rate stamps rather than printed indicia, some use PB meters. It's all about what generates better response vs. how much extra it costs -- period.

Anyway, recipients thought the Kraft paper envelope was from the IRS or some other ominous government agency, so they usually opened the envelope (which is the only purpose of any mailing envelope) -- and, FOOLED YA! . In focus groups, people always said how tricked they had felt and how they hated the piece for that, and would therefor never buy what was offered inside, but consistent good response rates belied those angry protestations. So much for believing what consumers say vs. how they actually behave.

Regarding the regrettable collateral damage of annoying those 98% of non-responding prospects: believe me, if there were a way mailers could identify in advance the 2% who will respond, they'd be doing it and saving themselves lots of money, not to mention trees. I hope the person who comes up with that methodology also invents an electronic filter to suppress only the crappy TV spots for local furniture stores and car dealerships (and also those cloying pharmaceutical spots), and leave alone the great ones (like the Miller Lite Playmates mud wrestling...).

Junk Male, my comment on the indicia was to indicate that if it's standard class, there is not account information enclosed and is therefore junk mail. I should have clarified that yes, there are standard class stamps and you can even meter for standard class, but my point was to look for the first class postage; if it's not there (stamp or meter and sometimes it's first-class presort, so it'll be $.29 or $.30), then no matter what the envelope says, it's 99% likely to be junk.

Oh, and you better believe I've used a first class stamp and paid to have letters hand-stamped instead of metered when I really want people to open the envelope, but it's only when I've got a really great offer that I believe will get a really great response. I don't want to waste a customer's time any more than I want to waste my budget. And I also stop mail to non-responders and rarely go deep in the database (unless I get pressure from high up). I'm nice like that (and I get very few DNM requests).

Hey Junk Male:

No one is "guessing" at the 2% response rate. Give some credit to people who do this stuff day in and day out. Get a hold of the annual DMA repsonse rate report and you'll see the (slghtly under) 2% rate for direct mail, years on end.